Serious overcapacity, consolidation of Chinese LED manufacturers is imperative

According to a survey by LEDinside, a green energy business unit of TrendForce, a global market research organization, since August last year, at least 5 cases of LED chip industry integration have occurred on both sides of the strait, including Jingdian ’s acquisition of the remaining 49% equity of Guangzhou Ga through equity transfer An Optoelectronics subscribed for 120 million ordinary shares of Canyuan Optoelectronics.

LEDinside said that since 2010, the Chinese LED chip industry's mad investment has led to a serious overcapacity of wafers, and product prices have continued to fall. Most companies have been struggling. The economy is picking up, and the overcapacity problem of the LED upstream chip industry cannot be alleviated in the short term, so industrial integration is an inevitable result.

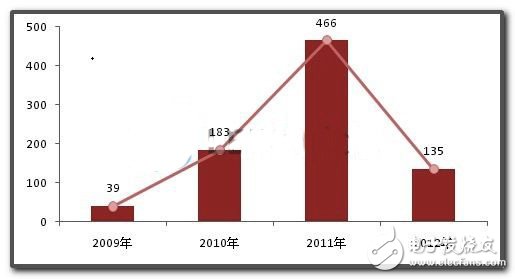

In 2009, the Yangzhou Municipal Government took the lead in introducing the MOCVD cash subsidy policy, and provided financial subsidies for new or expanded investment projects for the purchase of more than 5 new MOCVD equipment for the production of LED epitaxial wafers at one time. Subsequently, Jiangmen, Wuhu, Hangzhou, Wuhan and other local governments Launch a similar policy.

According to LEDinside statistics, as of the end of 2012, the number of Chinese MOCVD equipment has exceeded 900, but in 2012 China's MOCVD capacity utilization rate was less than 50%. The MOCVD subsidy policy directly led to new domestic LED epitaxial wafer projects popping up like mushrooms. According to statistics, from 2009 to 2012, a total of 65 new LED epitaxial wafer projects were established in China, but due to the harsh market environment, more than 30% of the projects have now been withdrawn or shelved.

The number of new MOCVD in Mainland China from 2009 to 2012 (Unit: Taiwan)

Overcapacity has led to increasingly fierce market competition. Furthermore, some chip companies have relied on government subsidies to adopt low-price market occupation strategies, which has directly led to a red sea in the chip market. The LEDinside survey found that domestic LED display screen chip prices fell the most severely in 2012, with some low-end product prices falling by 50%.

For example, Hangzhou Silan Optoelectronics, whose main business is display chips, had a gross margin of only 5.7% in 2012. LEDinside said that in 2012, most of the local LED chip companies in China were on the verge of loss, and some of the companies without financial support have fallen. The Chinese LED chip industry has changed from early technology competition to capital competition.

The gross profit margin of major Chinese LED chip manufacturers from 2010 to 2012)

* Remarks: Sanan Optoelectronics' 2012 gross profit margin refers to the gross profit margin of its LED business. Its LED business mainly includes LED chips and LED application products.

LEDinside pointed out that although the overcapacity problem caused by the investment boom is unlikely to be alleviated in the short term, from the trend of narrowing the decline in chip prices, some upstream companies have exhausted the cost of the bottom of the pressure box. The possibility of obtaining new financing has also been minimized.

On the other hand, the signal of industrial warming has also prompted some companies with relatively sufficient capital to have the courage to take another bet and acquire horizontal scale mergers through equity acquisitions to obtain the scale advantages needed for future competition. LEDinside expects that the integration of China's LED chip industry will accelerate in a large scale in the coming year.

Closed Tricycle Electric Vehicle

Three-Wheel Electric,Enclosed Electric Vehicle,Three-Wheeled Electric Vehicle,Closed Tricycle Electric Vehicle

Jinan Huajiang environmental protection and energy saving Technology Co., Ltd , https://www.hjnewenergy.com